This report summarises the key factors driving price changes at the end of the 2024, and into the new year:

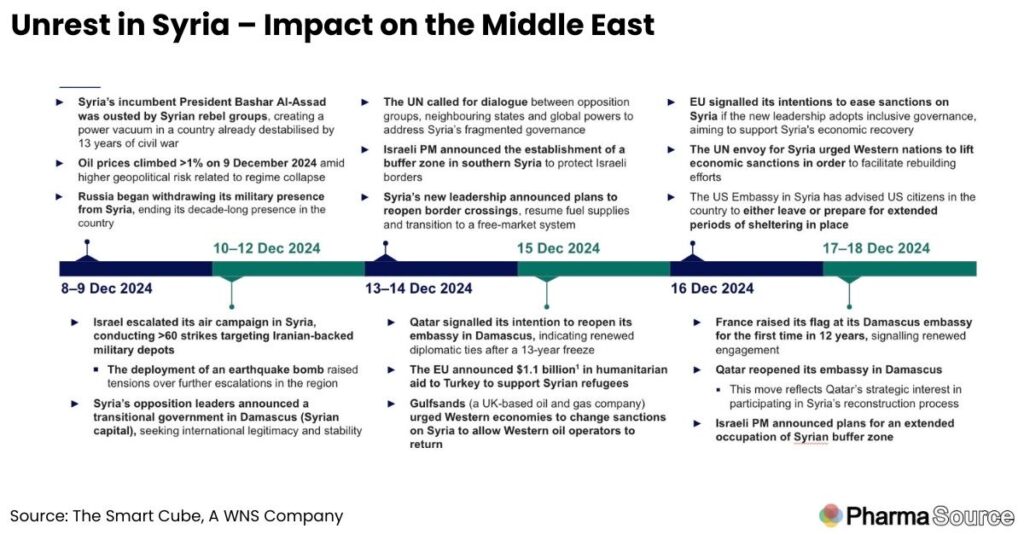

- On December 8, Syria’s incumbent President Bashar Al-Assad was ousted by Syrian rebel groups, potentially impacting Iran, Russia and other Western engagements in Syria.

- The BIOSECURE Act’s uncertain progress (now unlikely to pass this year as Congress heads into its holiday recess) along with Trump’s 10% tariff on Chinese imports, could raise contract manufacturing costs as US companies reduce reliance on Chinese suppliers, potentially increasing expenses but strengthening supply chain resilience.

- Bioprocessing supply prices remain volatile amid Middle East tensions, while lab supply costs may drop due to falling HDPE prices.

- In November 2024, Lupin Pharma and Aurobindo Pharma faced US product recalls due to cGMP violations, highlighting regulatory challenges for Indian pharma.

Biologics contract manufacturing

The global biologics contract manufacturing (biopharma CMO) market is expected to record a CAGR of 10.3% over 2025–2030, prompting increasing cost of services, driven by rising demand and the scaling of operations.

Pharma CDMOs are concentrating on increasing their capacity to broaden their service offerings and keep up with the rising demand; pharma companies are also entering the CDMO space to fulfil demand.

- In December 2024, Adragos Pharma (a Germany-based CDMO) announced the completion of a new ampoule filling line for $13.8 billion at its Livron-sur-Drôme site in France, to enhance its production capabilities.

- In December 2024, OneSource Specialty Pharma (an India-based CDMO) announced plans to expand its capacity to manufacture glucagon-like peptide-1 (GLP-1) drug-device combinations, as the demand for this new class of diabetes and obesity drugs rises globally.

Trump’s announcement (on 25 November) to impose an additional 10% tariff on all Chinese imports and the still likely introduction of the BIOSECURE Act aim to reduce reliance on Chinese suppliers, are compelling US-based companies to diversify sourcing activities and invest in domestic or alternative manufacturing.

- This may increase manufacturing costs but enhance supply chain resilience by reducing dependency on a single country and mitigating geopolitical risks.

Since Chinese CDMOs and other raw material manufacturers are a key source of relatively cheap contract manufacturing, the BIOSECURE Act holds the potential to increase the overall cost of biologics contract manufacturing in the US.

- Another potential issue related to the act is that CDMO and CRO capacity outside China may face challenges in meeting demand from the US and European pharma companies.

Bioprocessing Supplies

The single-use system (SUS) market is expected to witness a slight uptick in prices due to anticipated fluctuation in feedstock prices and steady demand; the cost is heavily dependent on the price of crude oil.

In November 2024, HDPE prices in the US decreased 5.1% M-o-M as compared with October 2024, while in Europe, the prices decreased 4.5% M-o-M to $1,491.2/tonne.

- The main factors behind this decline are reduced demand, lower feedstock ethylene prices, and oversupply, all of which have lowered production costs for HDPE.

- Disruption arising from escalations in the Middle East conflict can affect the bioprocessing supplies’ supply chain, as plastic and resin production, vital for SUS, heavily relies on crude oil.

- Disruption in crude oil supply directly affects plastics, thus impacting SUS manufacturing and potentially causing shortages and increased costs for pharma companies.

- Continued regional tensions, including the Israel–Iran conflict and attacks in the Red Sea, are disrupting the bioprocessing supply chain, as crude oil, a critical raw material for plastics and resin production, is vital for single-use systems (SUS).

Logistics and transport: Continued attacks in the Red Sea region have hampered the movement of goods, leading to delays in the shipment of key bioprocessing materials; major carriers and shipping companies have diverted routes to avoid high-risk areas, increasing transit times and costs for raw material deliveries.

Oil price fluctuations: In December 2024, the US EIA lowered its 2025 Brent crude oil price forecasts to $74/barrel from an average of $80/barrel in 2024, due to a decline in global demand and rising inventory levels amid increased production from non-OPEC countries; despite this decline, the volatility in oil prices continues to pose challenges for the bioprocessing industry.

The continued instability in the Middle East may lead to prolonged disruptions in supply chains, necessitating close monitoring and contingency planning.

Cell and gene therapy (CGT)

The CGT market witnessed steady activity in Q3 2024, marked by sustained deal volume, increased early-stage financing and regulatory progress.

- A total of 101 CGT deals were done in Q3 2024 compared to 100 deals in Q2 2024.

- The number of seed and Series A financing tripled to 19 transactions in Q3 2024 with an aggregate of $484.0 million – ~2x increase over the $266.3 million from Q2 2024.

- Q3 2024 saw 1 new approval across the CGT landscape with the approval of Adaptimmune’s Tecelra (afamitresgene autoleucel) by the USFDA for the treatment of synovial sarcoma.

Between Q4 2023 and Q3 2024, gene therapy clinical trials have increasingly focussed on non-oncology indications, marking a significant diversification in research focus; however, oncology continues to dominate the overall pipeline development.

- Non-oncology trials accounted for 39% of initiated trials in Q4 2023 and steadily increased to 51% by Q3 2024.

Regulatory compliance, submission and audit

Global pharma companies, particularly those based in low-cost countries, may need to allocate additional resources to comply with the stringent regulatory standards set by international bodies, especially the US FDA; this heightened scrutiny could result in increased compliance expenses, which may ultimately influence their pricing strategies.

- In November 2024, Lupin Pharma (an India-based pharma company) recalled 6,16,506 bottles of Ramipril capsules (used to treat high blood pressure) in the US, due to deviation from current good manufacturing practices (cGMP).

- In November 2024, Aurobindo Pharma (an India-based pharma company) recalled >1 lakh bottles of Cinacalcet tablets (used for the treatment of hyperparathyroidism) in multiple strengths, due to deviation from current good manufacturing practices (cGMP).

Small molecule manufacturing Chemicals and APIs

Donald Trump’s proposed tariff on Chinese imports and most favoured nation (MFN) status revocation could significantly disrupt the pharma industry, which relies heavily on Chinese APIs.

- This may increase costs, forcing companies to absorb losses or pass them on to consumers, while accelerating efforts to diversify supply chains; countries such as India and domestic API production could benefit as alternatives.

- Over the long term, initiatives, such as the BIOSECURE Act and localised manufacturing, are expected to improve supply chain efficiency, reducing reliance on international suppliers and stabilising costs.

API prices surged globally in November 2024 due to material shortages, production bottlenecks, rising demand, and stockpiling by manufacturers and distributors.

- Contributing factors include China’s manufacturing rebound driven by government stimulus, increased industrial input demand and India’s ability to pass escalating costs to consumers.

- Logistical issues, such as European and US port congestions and US labour strikes, further strained supply chains, driving API prices higher.

APU / Drug discovery and clinical trials

Wages account for >40% of the total cost involved in discovery and clinical research; due to the ongoing shortage of qualified and experienced researchers, operational costs will likely be high.

- The inflation rate rose in November 2024 in the US, potentially leading to temporary cost pressures.

- The inflation rate in the US rose to 2.7% in November 2024, vs. 2.6% in October 2024; annual inflation in the Euro area rose to 2.0% in October 2024, vs. 1.7% in September 2024.

Trump’s second term as the US President could accelerate drug approvals, increase clinical trial costs due to tariffs on Chinese imports, disrupt supply chains, and reshape vaccine research and public trust under new health policy leadership.

Medical devices

Post the 2024 US presidential elections, with Trump securing a second term, the medical devices industry is likely to experience significant changes, including the following:

- Streamlined US FDA approvals may accelerate innovation but will require increased investments in post-market monitoring and real-world evidence.

- Tariffs on Chinese imports may disrupt supply chains, driving diversification, while tax reforms could boost R&D and domestic manufacturing, though at higher costs.

Due to anti-corruption measures and weakened consumer confidence in China, med tech companies such as Philips has reduced its 2024 sales growth forecast, citing a significant decline in demand for its healthcare and medical devices.

In the past few months, the EU and US governments have tightened due diligence on China-based products, impacting medical device production and increasing costs.

- The US FDA has issued import bans on 4 Chinese manufacturers – Jiangsu Shenli Medical Production, Jiangsu Caina Medical, Zhejiang Longde Pharmaceutical and Shanghai Kindly Enterprise Development Group – due to quality concerns.

- The advance of the BIOSECURE Act to the US Senate may cause further bans on other China-based medical device manufacturers .

Analytical laboratory and processing equipment

The US PPI for analytical lab instrument manufacturing increased marginally by 0.2% M-o-M, while that of HVAC and commercial refrigeration equipment fell 0.4% M-o-M in November 2024.

- However, rising input costs for lab equipment and inflationary pressure have led India-based diagnostic labs such as Metropolis Healthcare and Dr. Lal PathLab to increase their service prices.

Diagnostic labs are expected to reassess their pricing strategies within 12–24 months.

Lab supplies and services

Declining HDPE prices are expected to drive down lab supplies costs, while rising aluminum prices and limited supply may push up primary packaging costs.

Plastic ware, glassware and reagents

~65% cost of manufacturing lab supplies is attributed to raw materials, which include HDPE, glass, polypropylene, etc.

- Further, the US PPI for chemicals and allied products decreased 1.5% M-o-M in November 2024.

- The global HDPE market saw a decline in November, especially in the US, European and Asian markets.

- In November 2024, HDPE prices in the US decreased 5.1% M-o-M as compared with October 2024, while in Europe, the prices decreased 4.5% M-o-M to $1,491.2/tonne.

The main factors behind this decline are reduced demand, lower feedstock ethylene prices, and oversupply, all of which have lowered production costs for HDPE.

Primary packaging

PVC/PET, glass and aluminium packaging

Blister packaging for pharma products typically involves raw materials, such as aluminium, PET and PVC, while HDPE is used for bulk drums.

- PVC suspension prices in the US remained stable at $0.46/lb in October 2024 as compared to September 2024.

- PET prices in Europe (Italy) also remained stable in November 2024, reaching $1,197.1/tonne.

- Aluminium prices are expected to rise during December 2024–January 2025 on account of a combination of high feedstock prices and low inventory levels (driven by bauxite supply disruptions from Guinea and Brazil, and strikes at the Bel Air terminal in Boffa).

Biologics and injectable drugs are typically packaged in glass or plastic vials/ampoules.

- The US PPI for flat glass manufacturing decreased by 1.0% in November 2024 compared to October 2024; this decrease may lead to a potential fall in prices across the broader flat glass category.

This category update is powered by The Smart Cube, a WNS Company. For more procurement intelligence, visit Amplifi PRO.