Alliance for Regenerative Medicine’s State of the Industry briefing at JP Morgan Healthcare Conference signals cautious optimism backed by $11.1B in 2025 funding

The cell and gene therapy (CGT) sector attracted $11.1 billion in investment across 216 financings in 2025—representing 18% of all biotech therapeutic deal value—despite emerging regulatory headwinds, according to Tim Hunt, CEO of the Alliance for Regenerative Medicine, who delivered the organization’s annual State of the Industry briefing at the JP Morgan Healthcare Conference on January 12, 2026.

Patient Impact is Irrefutable

Hunt opened by highlighting two patient stories that bookend the sector’s potential. Baby KJ Muldoon, who received a groundbreaking bespoke CRISPR treatment for a life-threatening disorder, represents the cutting edge of personalized medicine. At the other end of the spectrum, Marci McCue became the first patient dosed in a multiple sclerosis CAR-T trial in 2015 and shared her experience: “I don’t have to worry that I’m going to wake up tomorrow and lose function. That fear is not there anymore.”

Companies Adapt to Commercial Realities

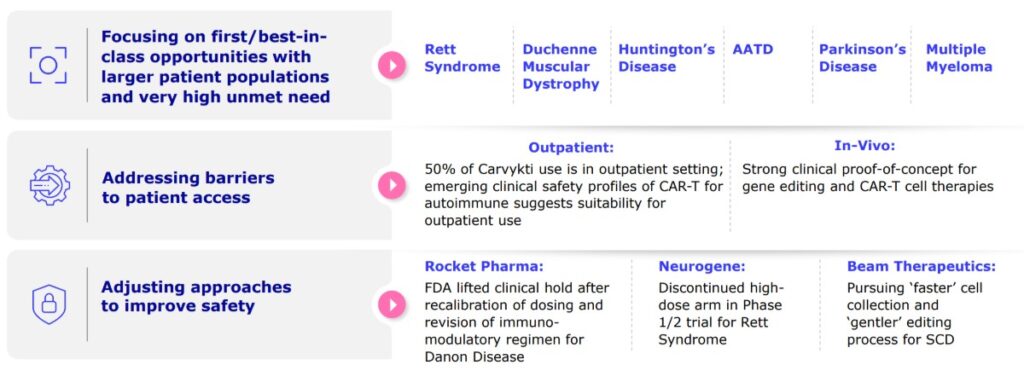

The sector has matured significantly in its approach to commercialization, Hunt argued. Companies are now:

- Focusing on larger patient populations with high unmet need, including Rett syndrome, Duchenne muscular dystrophy, Huntington’s disease, and Parkinson’s disease

- Addressing access barriers through outpatient treatment settings and in-vivo therapies

- Improving safety profiles through adjusted dosing and refined treatment protocols

Hunt drew a parallel to monoclonal antibodies, which followed a similar non-linear path to today’s $250 billion market as standard of care across many disorders.

Safety Data Provides Context

In a data-driven response to safety concerns that have plagued some AAV gene therapy programs, Hunt presented conservative mortality figures. Across the two largest AAV programs with 6,100 patients treated, only 14 publicly reported deaths have occurred—a mortality rate of 0.2%.

This compares favorably to mortality rates for comparable one-time interventions: auto stem cell transplants (2.8%), allo stem cell transplants (9.5%), heart transplants (3.6%), and liver transplants (3-5.9%).

“The benefits of AAV gene therapy often greatly outweigh the risks when you consider the conditions being treated,” Hunt stated, referencing continued progress in programs for Rett syndrome, Duchenne muscular dystrophy, and Danon disease.

Global Competition Accelerates Innovation

A striking revelation: For the first time in 2025, the Asia-Pacific region surpassed North America in clinical trials, with 990 trials versus 916. China led this surge, growing from 596 trials in the first half of 2025 to 716 by year-end—a 20% increase compared to the US’s 8% growth.

The European Union responded with its Biotech Act in December 2025, offering incentives including accelerated clinical trial timelines, ATMP centers of excellence, enhanced patent protections, and €10 billion in startup capital.

US Regulatory Landscape Shows Promise and Concern

Hunt expressed cautious optimism about the FDA under new leadership. HHS Secretary Robert F. Kennedy Jr. has publicly stated alignment between the “Make America Healthy Again” movement and cell and gene therapy’s goal of curing disease rather than managing chronic conditions.

Positive regulatory developments include:

- New CMC guidance offering manufacturing flexibility (announced January 11, 2026)

- Broader acceptance of real-world evidence

- Plausible mechanism of action pathway for gene editing

- CAR-T label updates and REMS program removal

- CMS embrace of the CMMI access model for state Medicaid programs

However, Hunt also outlined emerging concerns in the second half of 2025, creating an “OTP Scorecard” to track FDA performance. Questions include whether the Office of Therapeutic Products is adequately staffed, particularly in senior positions, and whether there’s an “unhealthy focus on methodological purity over regulatory flexibility for serious diseases.”

The scorecard already shows mixed results, with Atara Biotherapeutics receiving a Complete Response Letter on January 12, while several other programs await PDUFA dates in the coming months.

Commercial Opportunities Materialize

The sector added two new blockbusters in 2025: Carvykti (J&J) and Breyanzi (BMS), both CAR-T therapies showing explosive growth exceeding 100% year-over-year. Wall Street analysts expect these products, along with Zolgensma and Yescarta, to reach peak sales of $2 billion by 2031, with six additional blockbusters anticipated by that timeframe.

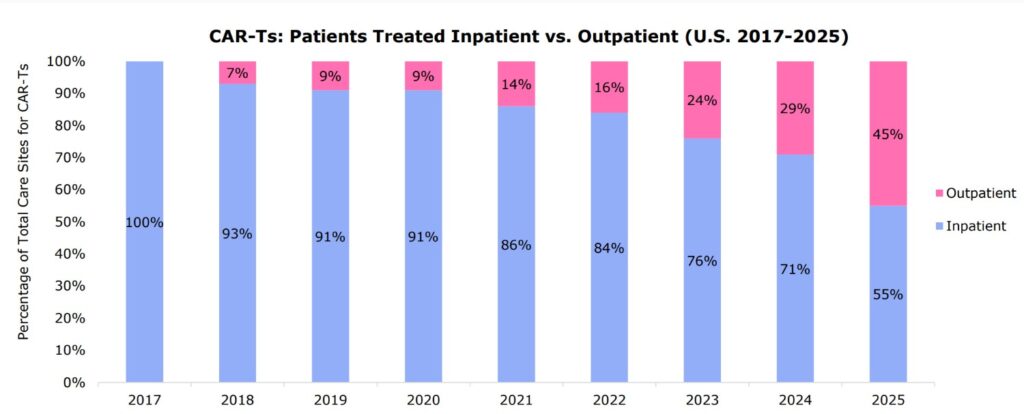

Hunt highlighted the growing outpatient trend for CAR-T therapies. In 2025, 45% of patients received treatment in outpatient settings, up from zero in 2017 and just 29% in 2024. Carvykti has achieved 50% outpatient utilization.

Twenty of the 30 largest biopharma companies by market cap are now actively developing or commercializing cell and gene therapies, with major players like BMS, Bayer, AstraZeneca, Regeneron, Gilead, Novartis, and Vertex working across multiple modalities.

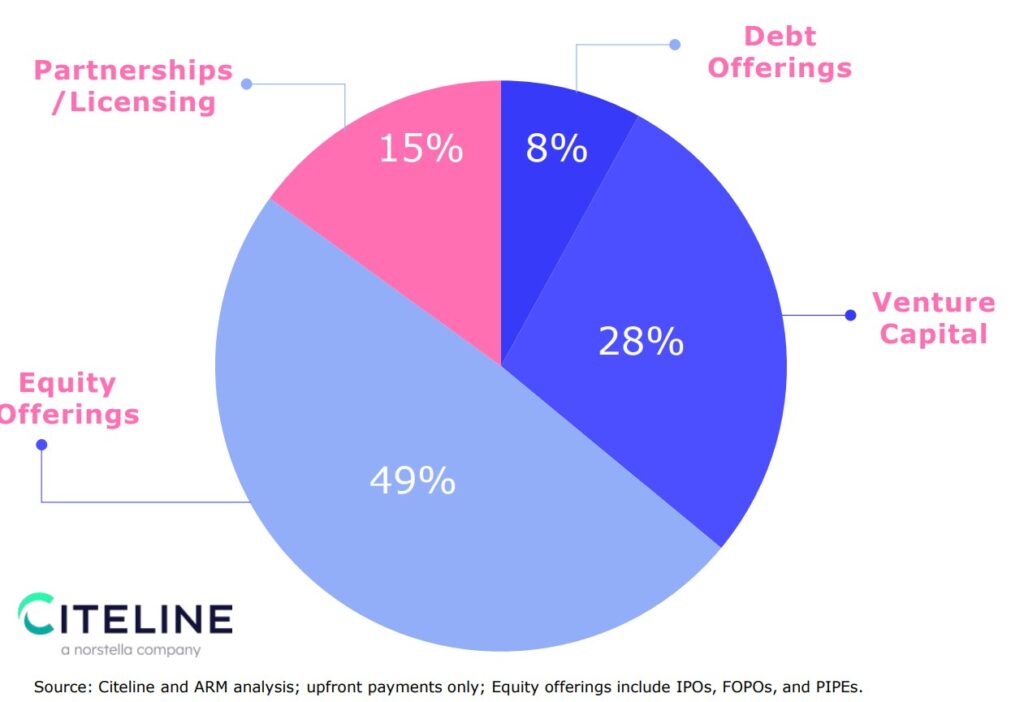

Investment Flows Remain Strong

Despite headwinds, the sector’s $11.1 billion in 2025 funding was distributed across venture capital (28%), equity offerings (49%), debt offerings (8%), and partnerships/licensing (15%).

Strategic acquisitions gained momentum, including AbbVie’s $2.1 billion purchase of Capstan Therapeutics, Bristol Myers Squibb’s $1.5 billion acquisition of Orbital Therapeutics, and Eli Lilly’s $1 billion upfront payment for Verve Therapeutics.

Cell and gene therapies comprised 23% of all biotech therapeutic deals and 18% of total deal value—up from 15% in 2024, according to data from Chardan.

Notable venture financings included Kriya Therapeutics ($320 million), Tune Therapeutics ($175 million), and Atsena Therapeutics ($150 million), demonstrating continued investor confidence across diverse technology platforms from gene therapies for larger populations to ocular conditions and tissue engineering.

Looking Ahead

Hunt outlined a robust near-term pipeline with six current regulatory decisions pending and at least 13 planned submissions across the US and Europe in 2026. Notable clinical milestones expected include Phase 3 data readouts for Duchenne muscular dystrophy, myasthenia gravis, retinitis pigmentosa, and wet AMD.

The sector’s evolution from early scientific promise through commercial challenges to emerging blockbusters mirrors the trajectory of monoclonal antibodies—suggesting that cell and gene therapies may be entering their own period of sustainable growth as standard-of-care treatments across multiple disease areas.

Watch the full presentation: