With only 64 sites in the Middle East-North Africa region supplying the U.S. market—representing just 1% of global API and finished dosage form capacity—the Iran conflict presents concentrated but manageable supply chain risk for most pharmaceutical companies. Here’s what we know.

The ongoing conflict between the United States, Israel, and Iran that began on February 28, 2026 has raised questions about pharmaceutical supply chain vulnerabilities in the region. While the Middle East-North Africa (MENA) region represents a small fraction of global pharma manufacturing capacity, the concentration of certain critical production creates specific exposure points worth understanding.

MENA’s Limited Role in U.S. Drug Supply

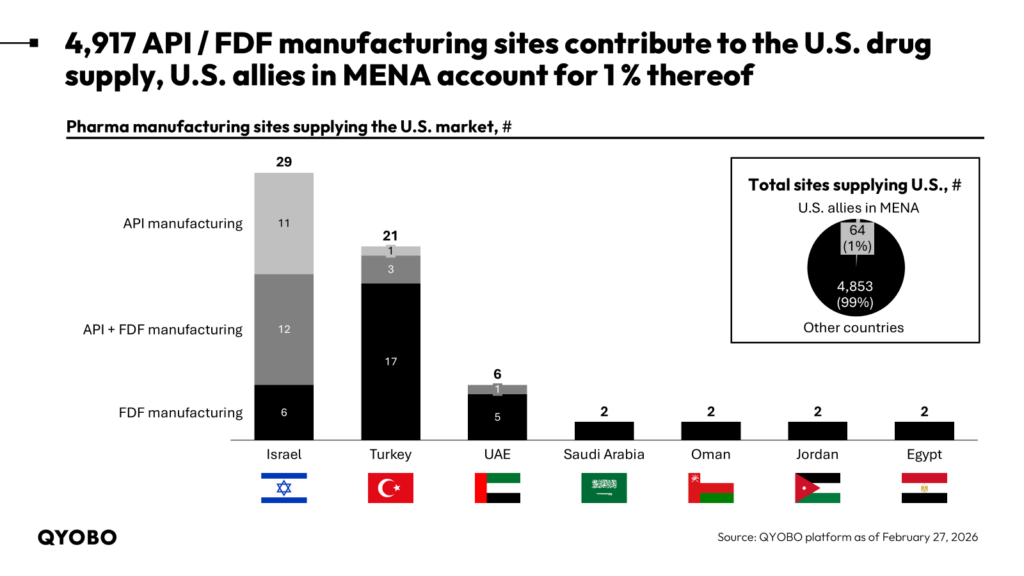

According to QYOBO platform data, only 64 manufacturing sites in U.S.-aligned MENA countries currently supply the U.S. pharmaceutical market—less than 1% of the 4,917 API or finished dosage form sites globally that serve the U.S.

The breakdown by country:

- Israel: 29 sites (11 API manufacturing, 12 API + FDF manufacturing, 6 FDF manufacturing)

- Turkey: 21 sites (3 API, 17 API + FDF, 1 FDF)

- UAE: 6 sites (all FDF)

- Saudi Arabia, Oman, Jordan, Egypt: 2 sites each

For most pharmaceutical companies, the region represents redundant supply—alternative sources exist for the vast majority of products manufactured there.

Single-Source Vulnerabilities

The meaningful supply chain risk lies in the small number of products with single-source manufacturing in the conflict zone. Based on supply chain mapping, at least two drugs (with a smaller patient population) are manufactured exclusively at a biologics facility in northern Israel. The specific therapeutics and manufacturer cannot be disclosed for patient safety reasons.

For the small patient populations dependent on these therapies—typically measured in hundreds to low thousands globally—alternative treatment options may be limited or nonexistent.