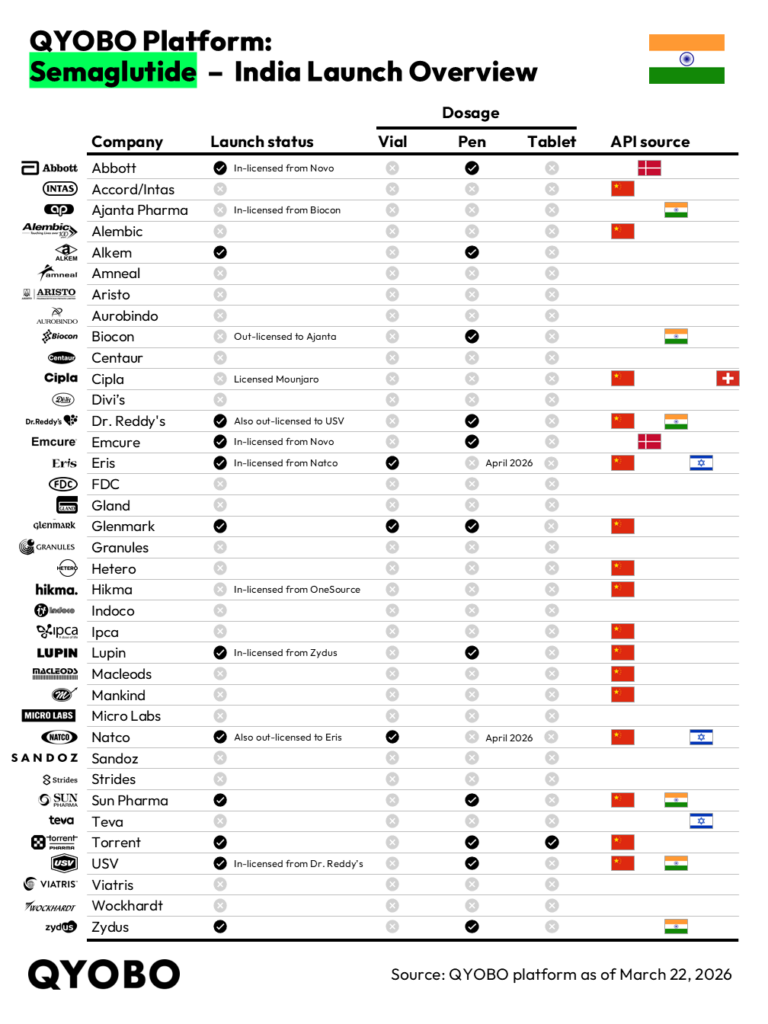

According to QYOBO’s India semaglutide launch tracking (March 2026), based on confirmed launch activity and licensing disclosures across India’s domestic pharmaceutical market, 13 companies are verified as active — significantly fewer than the 40-50 figure cited in media reports.

Media reports placed the number of companies launching semaglutide in India at 40 to 50. The confirmed figure is 13. Twelve companies launched on March 21, 2026, with Novo Nordisk joining to bring the active total to 13.

The 13 active players span a mix of direct manufacturers and licensing arrangements. Direct launchers include Alkem Laboratories, Dr. Reddy’s Laboratories, Glenmark Pharmaceuticals, NATCO Pharma, Sun Pharma, Torrent Pharmaceuticals, and Zydus. Five companies entered via licensing arrangements: Abbott and Emcure licensed from Novo Nordisk, Eris Lifesciences from Natco, Lupin from Zydus, and USV from Dr. Reddy’s. Broadening the lens to include GLP-1 agonists overall, Eli Lilly and Cipla — both offering tirzepatide — bring the total GLP-1 market participants to 15.

Pricing: Up to 35x Cheaper Than the Originator

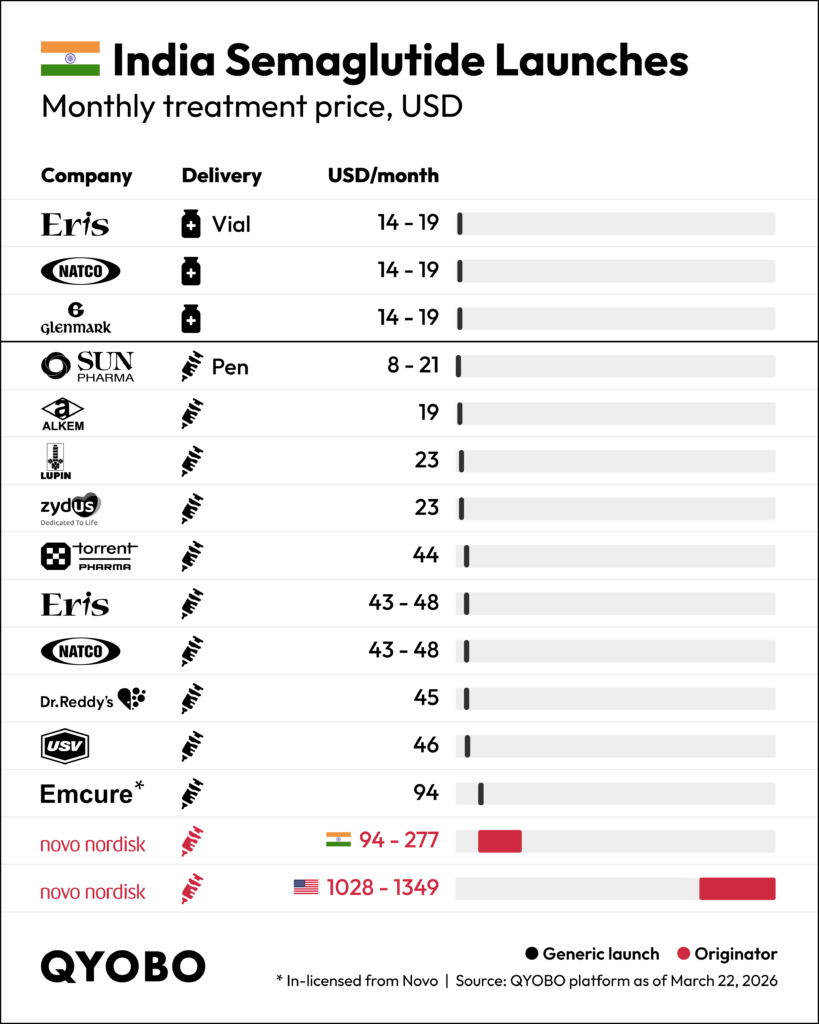

India is the first large-scale market where multiple semaglutide competitors have launched simultaneously, and initial price benchmarks are being set quickly. Monthly treatment costs among generics range from $8 to $48, with Sun Pharma entering at the lowest point ($8–$21/month) and Emcure — in-licensed from Novo Nordisk — at $94/month. Novo Nordisk’s own branded product in India runs $94–$277/month; in the U.S., the same product costs $1,028–$1,349/month.

Novo Nordisk manufactures both the API and finished dose in Europe and the U.S. Generic entrants are manufacturing finished dose domestically in India, predominantly using API sourced from China.

At the low end, generics are priced up to 35x below Novo Nordisk’s India price, and up to 170x below the U.S. price.

20 companies have purchased semaglutide API over the past 12 months, but have not yet launched. These companies are watching price erosion following the initial wave before committing. Most active players and API purchasers alike continue to source from China, making Chinese API supply a central variable in India’s GLP-1 economics regardless of how many domestic brands ultimately reach the market.

Canada, Brazil, and China are expected to see similar generic entries later in 2026. How competitors position their supply chains ahead of U.S. and European patent expiry will be the defining variable — and India’s pricing trajectory will serve as the first reference point.

Source: QYOBO, India semaglutide launch tracking, March 2026 — qyobo.com