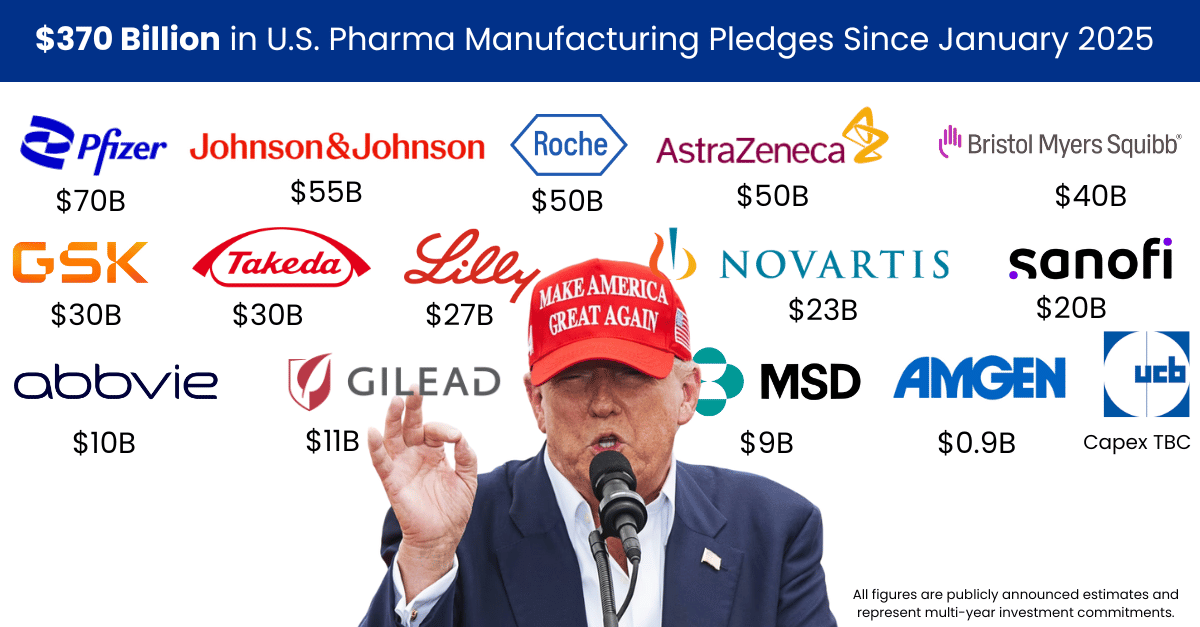

PharmaSource analysis of 732 industry announcements reveals massive investment in U.S. capacity, with partnerships dominating the news cycle and advanced therapy manufacturing reaching industrial scale

The pharmaceutical contract manufacturing landscape underwent a fundamental readjustment in 2025, marked by record investment flows, accelerated U.S. reshoring, and a decisive shift toward integrated technology platforms.

PharmaSource’s comprehensive tracking of 732 CDMO announcements throughout the year reveals an industry responding to geopolitical pressures, technological advances, and evolving sponsor demands with substantial speed and scale.

Download the full data set here

The $24.86 Billion Investment Wave

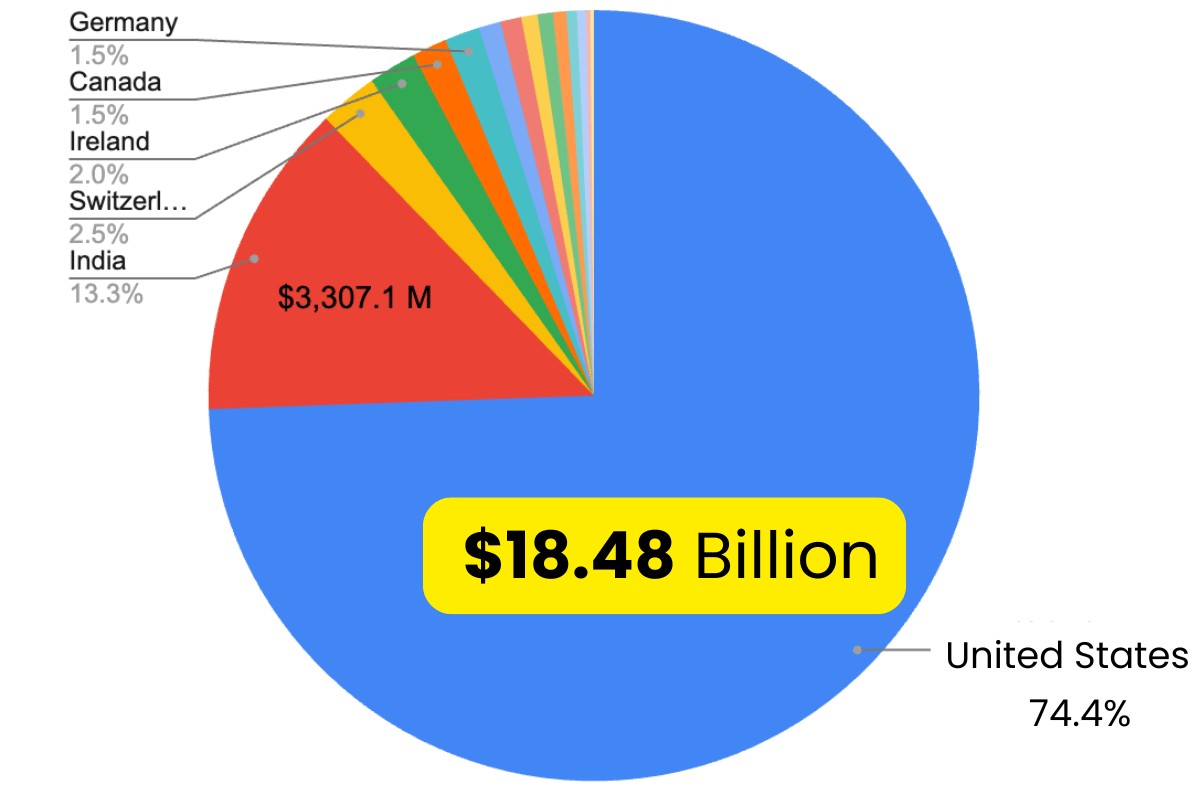

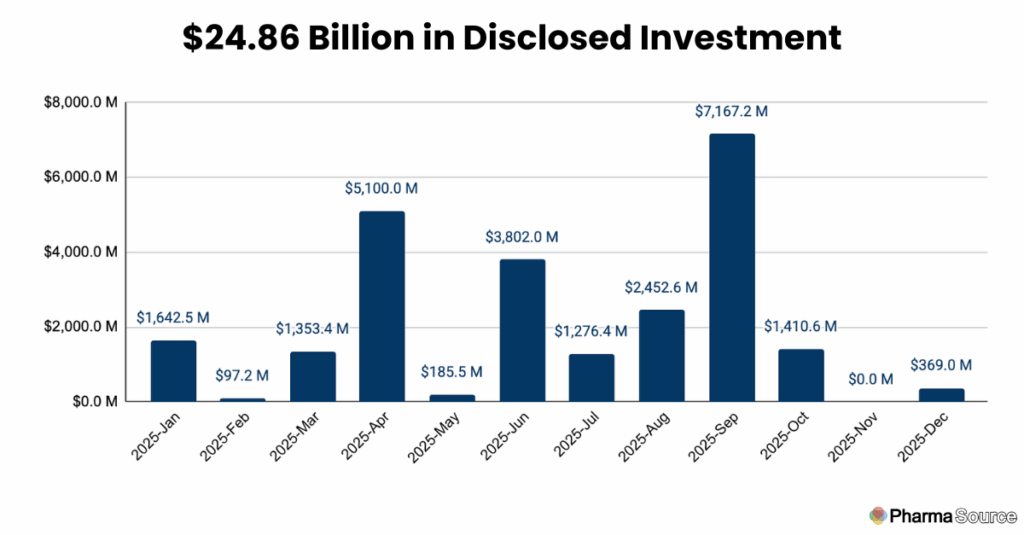

Total disclosed investment in CDMO capacity reached $24.86 billion in 2025, with September alone accounting for $7.17 billion—the highest single month of the year.

This investment wasn’t distributed evenly: 74% of all capital flowed to the United States, signalling a dramatic geographic concentration.

In an interesting parallel, according to Labiotech tracking, 74% of all biotech funding was directly within the United States in 2025.

The numbers tell a clear story. The U.S. captured $18.48 billion in disclosed investments, dwarfing India’s $3.31 billion (second place) and Switzerland’s $610 million (third). This represents a wholesale concentration of manufacturing capacity driven by supply chain security concerns, policy incentives, and sponsor preference for domestic production.

September’s Reshoring Acceleration

September crystallized the year’s defining trend with 81 total announcements—a 55% increase from August. In that single month, 97% of disclosed investment ($6.7 billion) flowed to U.S. facilities. Three announcements captured the scale of this shift:

FUJIFILM Biotechnologies officially opened its $3.2 billion Holly Springs facility in North Carolina, creating one of the world’s largest single-site biologics manufacturing campuses.

Toshihisa “Toshi” Iida, Chairman of FUJIFILM Biotechnologies, explained their growth strategy on the PharmaSource podcast:

“Current revenue scale is $1.3 billion. We anticipate it will grow to $5 billion, just in five years’ time. We’ve committed to invest about two-thirds of Fujifilm’s entire annual capex in this business.”

Samsung Biologics secured a $1.3 billion CDMO contract with an unnamed U.S. biopharma partner, demonstrating that large Korean manufacturers are successfully competing for domestic U.S. business.

Outside the U.S., significant investments continued in established biopharma hubs: PolyPeptide’s €100 million Malmö facility expansion in Sweden, AGC Pharma’s €110 million Barcelona expansion, Kindeva’s 150,000 square foot UK headquarters, and Delpharm’s $220 million Quebec investment with Canadian government support.

Partnerships Dominate: 301 Announcements

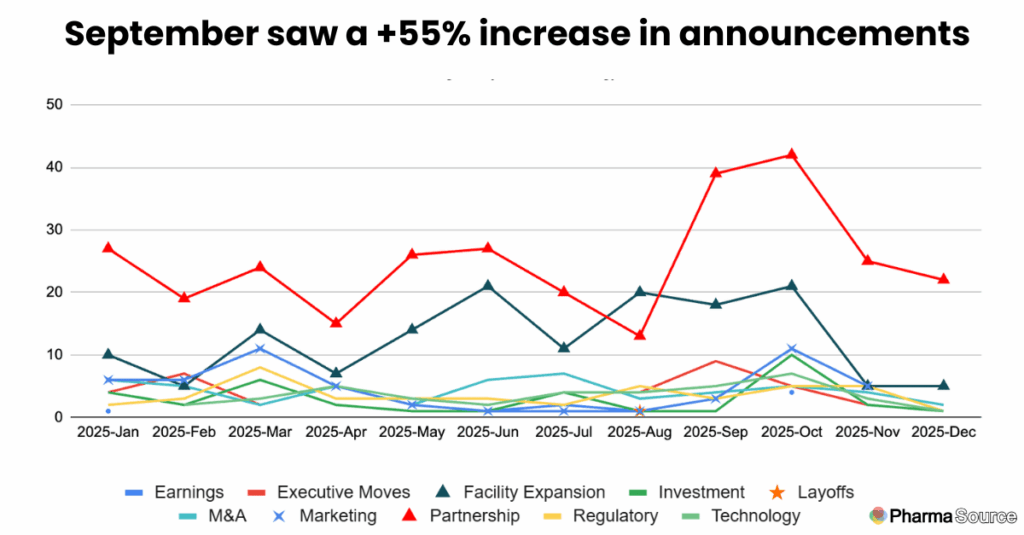

Partnerships were consistently the dominant announcement type throughout 2025, with 301 collaborations (41% of all news tracked). Month after month, partnerships led the news cycle, peaking at 42 announcements in October (38% of that month’s activity).

The partnerships cover both supply agreements and deeper strategic integration:

- Technology platform integrations: Charles River, incorporating Akadeum’s GMP T Cell Isolation Kit into its Flex platform; Integrated DNA Technologies partnering with Aldevron on Alt-R HDR Enhancer Protein for genome editing.

- Modality-specific collaborations: Multiple ADC (antibody-drug conjugate) partnerships as CDMOs race to build bioconjugation capabilities.

- Geographic expansion deals: Asian CDMOs partnering with European and U.S. firms to access regulated markets; Western CDMOs partnering with Asian manufacturers to access regional production capacity.

- End-to-end service integrations: CRO-CDMO partnerships offering seamless development-to-manufacturing transitions.

Facility Expansion: 154 Announcements Signal Capacity Building

The industry added significant new capacity in 2025, with 154 facility expansion announcements spanning:

- Biologics manufacturing: Multiple large-scale bioreactor installations, including Bora Biologics’ two 2000L bioreactors in San Diego, and expansions at LOTTE BIOLOGICS, Samsung Biologics, and WuXi Biologics sites globally.

- Fill-finish capacity: Responding to the injectable medicine surge, numerous CDMOs expanded aseptic filling capabilities, including Simtra BioPharma Solutions’ expansions across U.S. and European sites.

- Cell and Gene Therapy: Specialized facilities opened at Made Scientific (New Jersey), ProBio (New Jersey), and multiple European sites as CGT manufacturing moves from academic labs to industrial scale.

- ADC capabilities: Veranova, WuXi XDC, Cohance Lifesciences, and others expanded bioconjugation suites to capture growing ADC demand.

- Specialized modalities: Peptide synthesis (SK Pharmteco, PolyPeptide), oligonucleotides (BioSpring), and radiopharmaceuticals (multiple announcements).

The Most Active Players: Who Made the Most News

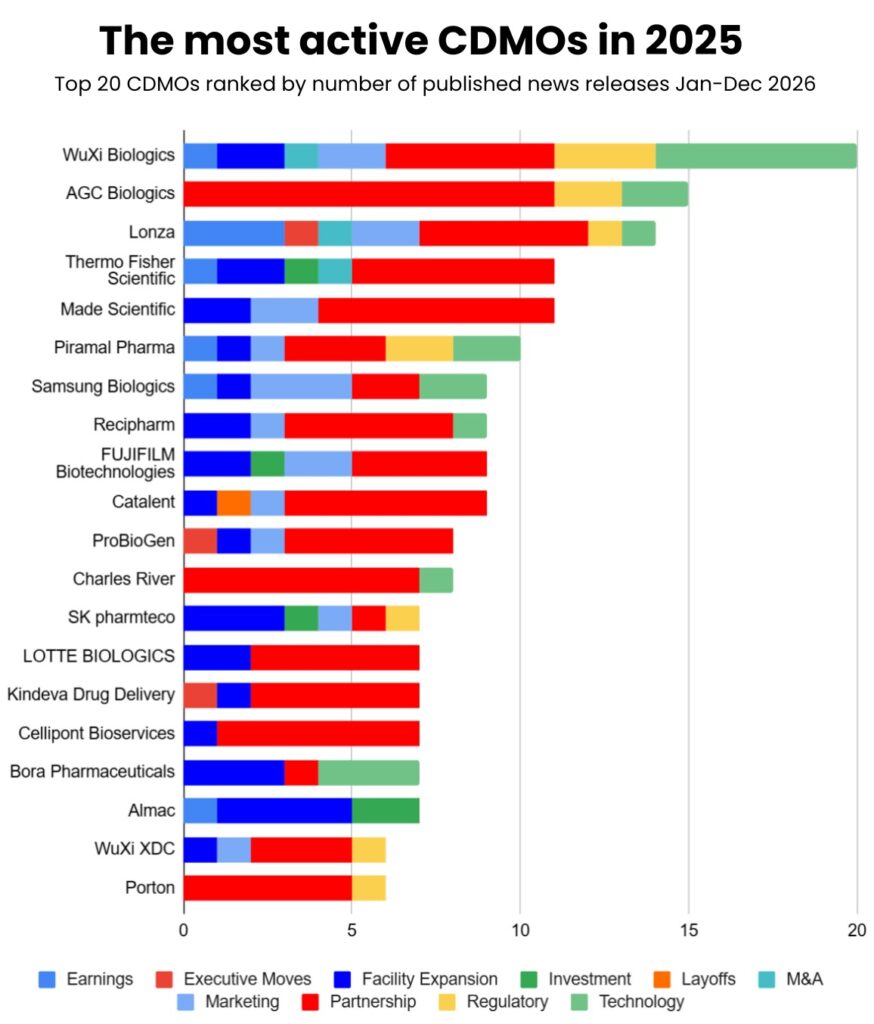

WuXi Biologics led all CDMOs with 20 announcements throughout 2025, despite ongoing U.S. legislative scrutiny. The Chinese CDMO maintained high visibility, announcing:

- Five facility expansions including Singapore and China sites.

- Six new technology platforms including TrueSite TI™ and WuXiHigh™2.0.

- Multiple regulatory approvals across global sites.

- Strategic partnerships with Qatar and Saudi Arabia to expand into new markets.

AGC Biologics followed with 15 announcements, positioning itself as a Western alternative with facilities across U.S., Europe, and Asia. Notable moves included launching a Cell and Gene Technologies Division and expanding services across its global network.

Lonza maintained high visibility with 14 announcements, with the launch of its One Lonza operating model to streamline global operations and including facility expansions, strategic acquisitions (Redberry SAS for QC testing).

Thermo Fisher Scientific made strategic moves including the $2 billion U.S. investment announcement and completion of Sanofi’s sterile fill-finish site acquisition, solidifying its position as pharma services market leader.

LOTTE BIOLOGICS, FUJIFILM Biotechnologies, Catalent, and ProBioGen each maintained active newsflow through 2025, demonstrating the breadth of competitive activity across the sector.

Technology Platforms: The New Competitive Differentiator

CDMOs competed on proprietary technology platforms rather than just manufacturing capacity. 2025 saw 39 technology announcements, including:

WuXi Biologics launched TrueSite TI™ Platform for accelerated biologics development and WuXiHigh™2.0 for high-concentration formulations—critical for subcutaneous delivery of biologics.

Abzena expanded its AbZelectPRO™ Platform with next-generation GS knockout systems for improved cell line development – as explained by their CSO in this recent podcast.

Samsung Biologics unveiled ExellenS™ to standardize manufacturing operations globally, promising consistent quality across its expanding network.

VectorBuilder unveiled its miniVec Plasmid System for safer, scalable genetic medicine manufacturing.

These platforms represent significant R&D investments and create switching costs for sponsors, potentially leading to longer-term relationships than traditional toll manufacturing arrangements.

The M&A Market: 51 Deals Reshape the Landscape

The industry saw 51 M&A transactions in 2025, ranging from bolt-on acquisitions to transformational deals:

Strategic exits: Sandoz’s planned acquisition of Just-Evotec Biologics EU SAS; Novartis divesting while Sandoz builds biosimilar manufacturing capability.

Capacity acquisitions: Syngene acquiring Emergent BioSolutions’ U.S. biologics facility for $50 million; Thermo Fisher completing acquisition of Sanofi’s sterile fill-finish site.

Technology tuck-ins: MilliporeSigma acquiring JSR Life Sciences’ chromatography business; PCI Pharma Services acquiring Ajinomoto Althea

Regional consolidation: Multiple deals in India, China, and Europe as regional players consolidated to compete with global CDMOs

Distressed assets: Some acquisitions reflected capacity coming back to market from overextended buildouts during the 2020-2022 boom

Geographic Patterns: The New Manufacturing Map

Beyond the U.S. dominance, the data reveal clear regional activity levels:

- United States (278 announcements): Overwhelming activity leader, capturing everything from mega-facilities to specialized niche capabilities. Policy support, sponsor preference, and supply chain security concerns all driving growth.

- United Kingdom (48 announcements): Europe’s most active market, benefiting from a strong life sciences sector, regulatory expertise, and government industrial strategy support.

- China (40 announcements): Maintained high activity despite U.S. policy pressures, with Chinese CDMOs expanding domestic capacity and pivoting toward Middle Eastern and Asian markets.

- India (38 announcements): Solidified position as center for small molecule and biosimilar manufacturing, with multiple facility expansions and growing biotech capabilities.

- Germany (34 announcements): Retained position as European biopharma hub, particularly for ADC manufacturing and specialized capabilities.

- South Korea (23 announcements): Samsung Biologics and LOTTE BIOLOGICS drove high activity, with both companies expanding domestically and internationally.

- Ireland, Switzerland, Japan: Each maintained steady activity, with established CDMOs in these markets expanding existing operations rather than greenfield development.

Modality Trends: Beyond Traditional Biologics

While traditional monoclonal antibodies remained the largest modality category, 2025 saw significant activity in emerging areas:

- Cell and Gene Therapy: 80+ announcements related to viral vector manufacturing, cell therapy processing, plasmid DNA production, and supporting capabilities. The modality is industrializing rapidly.

- ADCs (Antibody-Drug Conjugates): At least 30 partnerships and expansions focused on bioconjugation, payload production, or integrated ADC services. The approval of multiple ADC therapies drove commercial demand.

- mRNA and oligonucleotides: Continued buildout of lipid nanoparticle manufacturing, mRNA synthesis, and oligonucleotide production capacity following the COVID-era foundation.

- Radiopharmaceuticals: Growing niche with specialized facilities and partnerships emerging, particularly for oncology applications.

- Peptides: Multiple expansions in peptide synthesis capacity, driven by GLP-1 success and growing peptide therapeutic pipelines.

The modality diversity reflects drug development trends, with CDMOs building specialized capabilities rather than one-size-fits-all manufacturing.

Regulatory Developments: 43 Announcements

Regulatory approvals and inspections remained critical newsflow, with 43 announcements including:

- Multiple FDA facility approvals and zero-483 inspection outcomes

- EMA certifications for new facilities and expanded capabilities

- Chinese NMPA approvals for international CDMOs operating in China

- Specialty certifications like My Green Lab (sustainability) and various quality standards

The regulatory news reflects the maturing of newly built capacity, with many facilities announced in 2022-2023 now achieving operational approval in 2025.

What 2025 Reveals

2025 will be remembered as the year the CDMO industry’s geographic center of gravity decisively shifted westward. The $24.66 billion in disclosed investment, 301 partnerships consistently dominating the news cycle, and 154 facility expansions signal an industry in rapid evolution.

The 2025 data shows several clear patterns:

- U.S. capacity concentration is real with three-quarters of disclosed investment flowing to American facilities—a clear signal about where the industry sees its future.

- Partnerships drive the business with nearly half of all monthly announcements consistently focused on collaborations rather than independent capacity builds.

- Technology platforms matter with 39 platform announcements showing CDMOs differentiating on proprietary capabilities, not just manufacturing space.

- Geographic diversification strategies are evident, particularly among Asian CDMOs responding to Western policy pressures by building in multiple regions or serving domestic markets.

- Modality specialization is the strategy with CDMOs choosing to dominate specific technology platforms rather than trying to offer everything.

As 2026 begins, it remains to be seen how fast and how far the move will move towards US-based manufacturing, whether capacity can build fast enough to keep pace with demand, and whether this fast-moving and fragmented landscape will show any sign of consolidation in the year ahead.

North American CDMO Landscape infographic download

This analysis is based on PharmaSource’s comprehensive tracking of 732 CDMO announcements from January 1 through December 17, 2025, including partnerships, facility expansions, M&A transactions, investments, regulatory approvals, and technology developments. Download the full analysis here