The global peptide market stands at a pivotal moment in pharmaceutical development. After years of being considered challenging to manufacture and unstable for therapeutic use, peptides have emerged as one of the fastest-growing segments in the pharmaceutical industry.

Peptides are a growing class of drugs derived from polypeptides and used to treat a wide range of diseases. Many naturally occurring peptides act as hormones, growth factors, neurotransmitters, and anti-infectives, making them strong foundations for modern peptide-based therapies. Today, more than 100 peptide therapeutics have received FDA approval globally, including notable examples such as Tirzepatide (Mounjaro®), Lutetium Lu-177 vipivotide tetraxetan (Pluvicto®), and Lupkynis™.

The rising incidence of chronic conditions—including diabetes, obesity, osteoarthritis, autoimmune diseases, and cancer—is accelerating the demand for biologics. Peptides and recombinant proteins are increasingly preferred due to their high target specificity, favorable safety profiles, low toxicity, and reduced risk of off-target effects, reinforcing their expanding role in therapeutic development.

A peptide CDMO is a Contract Development and Manufacturing Organization that specializes in the synthesis, purification, formulation, and GMP-compliant production of peptide-based drug substances and drug products. These organizations combine deep chemistry expertise with scalable manufacturing infrastructure — from early-stage clinical supply through commercial production — enabling pharmaceutical and biotech companies to bring peptide therapeutics to market without building in-house synthesis capacity. As the global demand for therapeutic peptides accelerates beyond any previous forecast, partnering with the right peptide CDMO has become one of the most strategically critical outsourcing decisions in the pharmaceutical industry.

Peptides Market Trends-

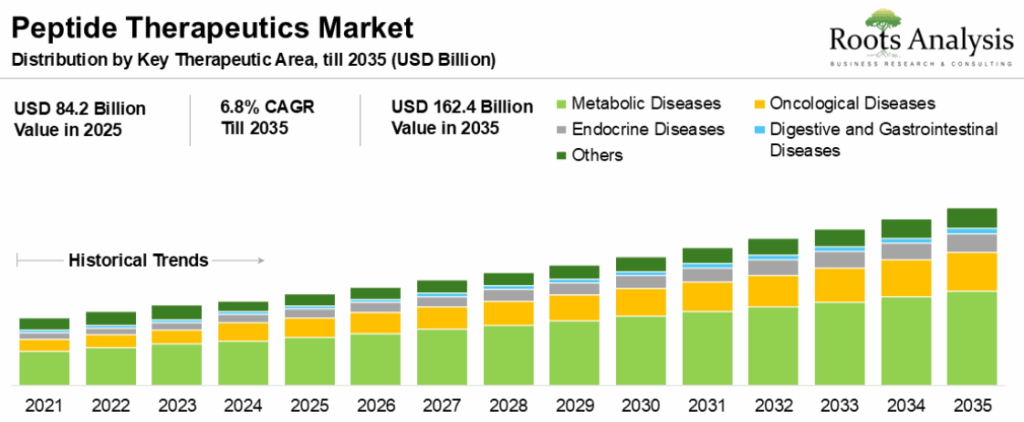

The peptides market reached USD 72.2 billion in 2024 and is projected to grow to USD 162.4 billion by 2035, representing a compound annual growth rate (CAGR) of 6.8%. Source- Roots Analysis

The global peptide market is entering a phase of explosive growth. This rapid expansion is fundamentally driven by two key factors: a surge in therapeutic demand and profound innovations in manufacturing and delivery. A primary market catalyst is the increasing global prevalence of obesity and related metabolic disorders, spotlighting the success of GLP-1 receptor agonists and the pipeline of drugs targeting related pathways says- Dr Wenyong Chen, SVP of ChemExpress CDMO.

This high-demand therapeutic area is significantly boosting the market value. Simultaneously, advancements in peptide manufacturing are making these complex molecules more accessible and affordable. For instance, the extensive application of biocatalysis in the synthesis of certain peptides, such as enlicitide, has resulted in an amazing reduction in production costs. This focus on cost-effective, sustainable production is crucial for enabling broader patient access. From a scientific perspective, the therapeutic strength of peptides lies in their modality advantage: they are particularly good to interact with flat protein-protein interaction (PPI) surface that are often considered “undruggable” by traditional small molecules. Finally, the convenience and patient compliance of peptide drugs are being revolutionized by formulation technology. Progress in developing oral tablet formulations is rapidly changing the landscape of peptide dosage, moving away from inconvenient injectables and making daily administration simpler for patients, thereby ensuring better adherence and treatment efficacy.

Three macro trends are currently reshaping the peptide CDMO landscape in ways that directly affect how sponsors approach outsourcing decisions.

GLP-1 demand surge – Rapid growth of obesity and diabetes drugs like semaglutide and tirzepatide is driving unprecedented demand for peptide CDMO capacity.

Expanding peptide pipeline – ~800 peptide drug programs globally (300 in clinical stages) are increasing outsourcing needs beyond metabolic diseases.

Rising molecular complexity – Longer, cyclic, stapled, and conjugated peptides require advanced synthesis platforms and specialized CDMO expertise.

What Are Peptides?

Peptides are chains of amino acids linked by peptide bonds, typically ranging from 2 to 50 amino acids in length. These molecules occupy a unique therapeutic space between small molecule drugs and large biologics, offering the specificity of antibodies with better tissue penetration and lower manufacturing complexity.

The human body naturally produces over 7,000 known types of peptides that serve as hormones, neurotransmitters, growth factors, and signaling molecules. Pharmaceutical peptides are either isolated from natural sources or, more commonly today, synthesized in laboratories using recombinant DNA technology or chemical synthesis methods.

Dr. Alaric Desmarchelier, Business Development Manager – Peptides at Almac Sciences, shares his perspectives on the evolving peptide therapeutics landscape.

Peptides are gaining prominence as a therapeutic class due to their high specificity, low toxicity, and ability to mimic natural biological processes more effectively than small molecules. These characteristics make them suitable for treating a wide range of diseases.

The peptide therapeutics market is growing rapidly, driven by increasing demand for targeted treatments for chronic conditions such as diabetes, cancer, and obesity. The global market was valued at around USD 49.7 billion in 2025 and is projected to reach USD 100 billion by 2034. Manufacturing technologies are also evolving. Peptides are mainly produced using recombinant methods or solid-phase peptide synthesis (SPPS), while liquid-phase peptide synthesis (LPPS) is gaining traction for better scalability, cost efficiency, and reduced environmental impact. The peptide synthesis market is expected to grow from USD 2.8 billion in 2025 to USD 5.1 billion by 2035, supported by more than 75 CDMOs offering peptide API manufacturing, highlighting the growing outsourcing trend. Innovation is further expanding the field, with peptide candidates emerging in immunotherapies, radiopharmaceuticals, and CNS treatments. Advances in oral delivery technologies, along with techniques such as PEGylation and fatty acid conjugation, are improving peptide stability, extending half-life, and enhancing patient compliance.

How Peptides Work

Peptide drugs function through several mechanisms. Most bind to specific cell surface receptors with high affinity and selectivity, triggering or blocking intracellular signaling pathways. This targeted approach allows peptides to modulate biological processes with precision that traditional small molecules often cannot achieve.

For example, glucagon-like peptide-1 (GLP-1) receptor agonists like semaglutide bind to GLP-1 receptors in pancreatic beta cells, stimulating insulin secretion in a glucose-dependent manner. This mechanism treats type 2 diabetes while minimizing hypoglycemia risk. These same drugs also act on receptors in the brain to reduce appetite, leading to their approval for obesity treatment.

Other peptides work as enzyme inhibitors, antimicrobial agents, or delivery vehicles for other therapeutic payloads. Peptide-drug conjugates represent an emerging class that combines the targeting specificity of peptides with cytotoxic agents for cancer treatment.

Pharma Trends: Oncology, GLP-1 Expansion, and AI-Driven Development Ryan Quigley, CEO of Inizio, highlights oncology, GLP-1s, and immunology as the fastest-growing therapeutic areas over the next five years.

GLP-1s Expanding Beyond Obesity While GLP-1 demand in obesity and diabetes is well established, Quigley expects the mechanism to reshape multiple adjacent categories. He notes active development in early Alzheimer’s disease, NASH, sleep apnea, cardiovascular disease, renal disorders, and other obesity-related comorbidities.

The commercial implications are significant. GLP-1 therapies will expand beyond specialist settings into much broader patient populations, requiring new go-to-market strategies. Companies will need more sophisticated marketing models and diversified engagement approaches to reach both physicians and consumers at scale.

Treats short bowel syndrome, graft-versus-host disease, IBD

Cardiovascular Disease

Regulate blood pressure and heart failure

Prevent thrombosis via vascular receptor targeting

Neurological Disorders

Target Alzheimer’s, Parkinson’s, and neurodegenerative diseases

First peptide treatment for Rett Syndrome (2023)

Infectious Diseases

Antimicrobial peptides fight resistant bacteria and viruses (e.g., HIV)

Endocrine Disorders

Synthetic hormones (insulin, GH, PTH) for endocrine deficiencies

Growth Factors Driving Market Expansion

Rising Chronic Disease Burden

According to the WHO, in 2022, an estimated 20 million new cancer cases were reported globally, resulting in 9.7 million deaths. Approximately 53.5 million people were living within five years of a cancer diagnosis. The Centers for Disease Control and Prevention reports that over 129 million Americans suffer from at least one chronic illness, including diabetes, obesity, heart disease, and hypertension.

The global diabetes epidemic represents a massive market opportunity. It is estimated that over 1.31 billion people will have diabetes globally, with approximately 44.7% of adults unaware of their diabetic condition. Peptide-based GLP-1 receptor agonists have become frontline therapies for type 2 diabetes and obesity, driving unprecedented demand.

Technological Advancements in Synthesis

Modern peptide synthesis technologies have overcome historical limitations. Solid-phase peptide synthesis (SPPS), first developed in the 1960s, has been refined with automated synthesizers, microwave-assisted chemistry, and advanced coupling reagents that dramatically improve yield and purity.

Hybrid synthesis strategies combining SPPS with solution-phase fragment condensation enable production of longer, more complex peptides previously considered impractical. Recombinant DNA technology allows biological production of certain peptides in microbial or mammalian cell systems, offering advantages for post-translational modifications.

Chemical Modifications Enhancing Drug Properties

Chemical modifications have transformed peptides from short-lived molecules requiring frequent injections into long-acting therapeutics suitable for weekly or monthly administration. Key strategies include:

PEGylation: Attachment of polyethylene glycol chains increases molecular size, reducing renal clearance and extending half-life

Lipidation: Addition of fatty acid chains enables albumin binding, prolonging circulation time

Cyclization: Creating cyclic structures improves proteolytic stability and membrane permeability

Stapling: Introducing chemical crosslinks stabilizes peptide secondary structure

D-amino acid substitution: Replacing natural L-amino acids with D-isomers at specific positions enhances resistance to enzymatic degradation

Improved Delivery Systems

Advances in drug delivery have expanded peptide administration routes beyond injection. While parenteral delivery remains dominant, accounting for over 84% of peptide therapeutics, oral formulations are emerging. The topical route of administration is projected to grow at a CAGR of approximately 30% during the forecast period.

Oral peptide delivery strategies include enteric coatings, permeation enhancers, protease inhibitors, and nanoparticle encapsulation. These technologies protect peptides from gastric degradation and facilitate intestinal absorption.

Personalized Medicine Integration

The FDA’s Center for Drug Evaluation and Research approved 16 new personalized treatments for rare diseases in 2023, a significant increase from 6 approvals in 2022. Peptides’ modularity and ease of customization make them ideal candidates for personalized therapies tailored to individual patient genetic profiles.

Strong Clinical Pipeline

More than 60 peptide drugs have received FDA approval, with over 150 peptide-based therapeutics in clinical trials. According to EUROAPI in October 2022, there are 500 peptide molecules currently in development, with expectations that 30 would receive approval by 2025.

The robust pipeline spans diverse therapeutic areas, with oncology research surpassing diabetes as a key area for peptide drug development in recent years. Immune checkpoint inhibitor peptides are gaining prominence for their potential to revolutionize cancer immunotherapy.

Growth Inhibitors and Market Challenges

Manufacturing Scale-Up Complexity

Peptide manufacturing presents unique technical challenges that limit production efficiency and increase costs. Unlike small molecules synthesized through a few chemical steps, peptides require sequential addition of amino acids, with each coupling step introducing potential for errors.

Tight labor markets have doubled average recruitment lead times for senior chromatographers, inflating project timelines and driving salary inflation well above market averages. The specialized expertise required for peptide chemistry, purification, and analytical characterization creates workforce shortages that constrain industry expansion.

Process Yield and Purity Issues

Each amino acid coupling in solid-phase synthesis proceeds with less than 100% efficiency. For longer peptides, cumulative coupling failures produce truncated sequences and deletion peptides as impurities. This phenomenon limits practical SPPS to approximately 50-70 amino acids, even with optimized chemistry.

Achieving pharmaceutical-grade purity (typically ≥95%) requires advanced preparative high-performance liquid chromatography (HPLC). Scaling these purification methods from milligram to kilogram quantities demands sophisticated equipment and process optimization. Peptide aggregation during synthesis, purification, or storage represents a persistent quality concern requiring careful control of pH, temperature, and solvent conditions.

High Production Costs

Peptide manufacturing remains expensive compared to small molecule production. Protected amino acids, coupling reagents, and high-purity solvents represent significant material costs. Large-scale SPPS requires specialized reactors, expensive resins, and substantial solvent volumes.

Labor-intensive purification and quality control further increase costs. Multi-column preparative chromatography, lyophilization, and comprehensive analytical testing add substantial expense. These high production costs translate to higher drug prices, potentially limiting patient access despite clinical benefits.

Supply Chain Vulnerabilities

Capital-intensive expansions across the CDMO sector signal an industry working to alleviate capacity bottlenecks while simultaneously navigating sustainability pressures from solvent-intensive peptide synthesis. Major facilities in Switzerland, Colorado, Belgium, and Sweden are undergoing multi-hundred-million-euro upgrades to meet surging global demand.

Commercial-scale peptide synthesis consumes large quantities of protected amino acids, resins, and specialty reagents. Disruptions to global supply chains can delay production and increase costs. Dependence on limited suppliers for exotic amino acids or specialized reagents creates risk.

Regulatory Complexity

Divergent FDA and EMA review frameworks create duplicative data packages for peptide-oligonucleotide conjugates, adding uncertainty to chemistry, manufacturing, and controls (CMC) planning. Different regulatory expectations regarding impurity characterization, analytical methods, and stability testing require flexible manufacturing processes and increase development timelines.

Peptide-specific regulatory guidance continues to evolve. Immunogenicity assessment requirements, particularly for modified peptides and peptide-drug conjugates, add complexity to clinical development programs.

Short Half-Life and Stability Issues

Despite advances in chemical modification, many peptides retain relatively short half-lives in vivo due to proteolytic degradation and renal clearance. This necessitates frequent dosing or complex formulation strategies, reducing patient convenience and potentially limiting market adoption.

Physical and chemical instability during storage remains challenging. Peptides can undergo aggregation, oxidation, deamidation, and other degradation pathways. Maintaining stability throughout manufacturing, distribution, and patient use requires refrigerated storage and careful formulation development.

Contract Manufacturing for Peptides

Unique CDMO Challenges in Peptide Manufacturing

Contract manufacturing of peptides presents distinct challenges compared to small molecules or biologics, requiring specialized expertise and infrastructure.

Technical Complexity and Process Development

Peptide synthesis involves iterative chemical steps—deprotection, coupling, washing—repeated for each amino acid addition. Optimizing reaction conditions, reagent stoichiometry, and cycle times for each peptide sequence demands extensive process development.

Transitioning from laboratory-scale synthesis to commercial production is non-linear. Industrial-scale facilities now possess large SPPS vessels ranging from several thousand to ten thousand liters, with some recognized as the largest peptide API producers worldwide. The addition of extra-large synthesis vessels significantly increases assembly time, capacity, and flexibility, enabling manufacture of complex long peptides with outputs reaching hundreds of kilograms per single batch.

Scaling requires revalidation of mixing efficiency, heat transfer, and solvent handling at larger volumes. Minor variations in reaction conditions can significantly impact yield and impurity profiles at commercial scale.

Analytical Method Development

Peptide characterization requires sophisticated analytical techniques. High-resolution mass spectrometry confirms molecular weight and detects sequence variants. Reversed-phase HPLC separates closely related impurities. Amino acid analysis verifies composition. Peptide mapping using enzymatic digestion confirms sequence and detects modifications.

CDMOs must develop and validate peptide-specific analytical methods for identity, purity, potency, and stability assessment. Product complexity is rising as multimodal peptide-oligonucleotide conjugates move from research to clinic, demanding new analytical expertise and pushing CDMOs toward end-to-end service models that include process development, fill-finish, and regulatory support.

Quality Control and GMP Compliance

Pharmaceutical peptide manufacturing must comply with current Good Manufacturing Practices (cGMP), requiring extensive documentation, validated processes, and quality systems. CDMOs must maintain change control procedures, deviation management, batch records, and stability programs.

Environmental monitoring, equipment qualification, and personnel training programs ensure consistent quality. Regulatory inspections by FDA, EMA, and other authorities assess compliance with cGMP standards.

Formulation and Fill-Finish Challenges

Most peptide therapeutics are administered by injection, requiring sterile formulation and aseptic filling. Peptides may require lyophilization (freeze-drying) to improve stability, adding complexity and cost.

Developing stable formulations involves selecting appropriate buffers, pH, excipients, and storage conditions. Compatibility with container closure systems must be demonstrated. Pre-filled syringes and autoinjectors improve patient convenience but require specialized filling equipment and validation.

Sustainability Considerations

CDMOs navigate sustainability pressures from solvent-intensive peptide synthesis. SPPS consumes large volumes of dimethylformamide (DMF), dichloromethane (DCM), and other solvents. Environmental regulations and corporate sustainability goals drive efforts to reduce solvent usage, implement recycling programs, and adopt greener chemistry.

Waste disposal costs and environmental impact represent growing concerns. Solvent recovery systems, aqueous purification methods, and enzymatic synthesis approaches offer potential solutions, though implementation at commercial scale remains challenging. Major European facilities are investing heavily in sustainable peptide manufacturing infrastructure to address these environmental challenges.

Selecting a peptide CDMO is one of the highest-stakes outsourcing decisions in pharmaceutical development. Unlike generalist biologics CDMOs, peptide specialists must possess a specific combination of synthesis chemistry, purification science, and formulation expertise that varies significantly across peptide types and sequence complexity levels. The following eight criteria should anchor every peptide CDMO evaluation.

Synthesis capability – CDMO should have proven experience with your peptide type (linear, cyclic, conjugated) and scale, including difficult sequences.

GMP capacity – Confirm available manufacturing slots and ability to support clinical-to-commercial scale.

Purification capability – Ensure adequate HPLC capacity and ability to consistently achieve >98% API purity.

GLP-1 capacity impact – Verify how much CDMO capacity is committed to GLP-1 programs and availability for new projects.

Formulation expertise – Capabilities in injectable peptide formulation, lyophilization, and ideally integrated fill-finish.

Regulatory track record – Experience with IND/NDA/DMF filings and strong FDA/EMA inspection history.

COGS transparency – Clear pricing model and cost structure across clinical and commercial scales.

Dr. Alaric Desmarchelier, Business Development Manager – Peptides at Almac Sciences, offers best-practice insights on how sponsors can get the most out of CDMO partnerships in this market.

Peptide drug development presents unique challenges including increasingly complex synthesis, stringent and evolving regulatory requirements, and scale-up hurdles that make CDMO partnerships critical. Sponsors should focus on early engagement, technical expertise, and a philosophy and capacity adapted to the drug candidate

1. Engage Early and Define Scope Clearly Peptide projects often involve intricate chemistries such as cyclic structures, disulfide-rich scaffolds, and conjugates like GLP-1 agonists. Sponsors should involve CDMOs at the preclinical stage to leverage their expertise in route scouting, route selection and analytical release testing. Early collaboration ensures robust Chemistry, Manufacturing, and Controls (CMC) planning and mitigates risks during scale-up for clinical and commercial phases.

2. Prioritise Technical and Regulatory Competence Select CDMOs with proven capabilities in handling complex peptides, and beyond. These modifications demand specialised purification and analytical methods to achieve high purity and regulatory compliance, often blurring the line between small and large molecules in terms of technical know-how. Sponsors should verify CDMO experience and licencing status in GMP manufacturing and global regulatory frameworks, as peptide drugs require specific and rigorous release and stability testing.

3. Philosophy and capacity fit Successful partnerships hinge on transparency and structured governance. Established project teams, prompt and expert communication between parties, clear escalation pathways, and quality agreements aligned with ICH and FDA standards are a must. Continuous dialogue on timelines, capacity constraints, and risk-sharing models is essential. IP considerations should not be neglected – select a CDMO with a clear IP position on processes, with which you are comfortable. Likewise, documentation practices should be scrutinised with the view that your process might have to move elsewhere or onboard additional manufacturers in the future. Finally, capacity fit is crucial: does the CDMO have a proven track record for the scales and technical requirements being discussed? Is the project a right fit for their know-how? Are they willing to learn & develop if required?

Best Practices for Maximizing Value from Peptide CDMO Partnerships

Wenyong Chen, SVP of ChemExpress CDMO, emphasizes that sponsors should take a strategic, long-term, and collaboration-focused approach when working with peptide CDMOs. The key is to align precisely on capacity needs—most peptide therapeutics require only small commercial volumes, so sponsors should look for CDMOs whose scale and cost structure fit these lower-kilogram demands rather than large, generic capacity claims.

He also stresses the importance of choosing partners with true end-to-end capabilities. Peptides frequently involve unnatural amino acids and complex modifications, making it essential to select a CDMO that can manage everything from regulatory starting materials through commercial GMP manufacturing. This avoids costly tech transfers and reduces operational risk.

For emerging modalities like peptide conjugates, Chen advises ensuring the CDMO can handle all components in-house—the carrier, linker, payload, and conjugation process. Such integrated expertise shortens timelines, streamlines the supply chain, and significantly lowers development risk.

Due Diligence Process

Selecting a peptide CDMO warrants thorough due diligence:

Request for Information (RFI): Issue detailed questionnaires covering technical capabilities, capacity, quality systems, and experience

Site Audits: Visit facilities to assess infrastructure, equipment, and operations firsthand

Technical Discussions: Engage CDMO scientists in detailed conversations about synthesis strategies and analytical approaches

Quality System Review: Examine standard operating procedures, batch records, and quality metrics

Regulatory Assessment: Review inspection history and regulatory filing experience

Client References: Contact current and former clients about their experiences

Financial Stability: Assess the CDMO’s financial health and ownership structure to ensure long-term viability

Red Flags to Watch

Certain warning signs should prompt careful consideration or disqualification:

Reluctance to provide references or allow site visits

Recent regulatory warning letters or import alerts

High staff turnover in key positions

Outdated equipment or facilities in poor condition

Vague or evasive responses to technical questions

Unrealistic promises regarding timelines or capabilities

Lack of experience with peptides of similar complexity

Insufficient capacity or unclear expansion plans

Before signing with any peptide CDMO, every sponsor should ask:

What percentage of your current and planned SPPS capacity is committed to GLP-1 programs, and what is genuinely available for a new client starting within our required timeline?

What is the longest and most complex sequence you have manufactured at GMP scale, and can you provide batch records demonstrating purity above 98% and a full impurity profile?

Do you manufacture your own amino acids and reagents, or source them externally — and what is your contingency plan if a primary reagent supplier encounters supply disruption?

How many peptide drug substance INDs and NDAs have you supported as the manufacturing site of record, and can you provide references from the regulatory teams involved?

And: what is your technology transfer process from clinical to commercial scale, and can both stages be completed within the same facility?

Decision Framework

Create a structured evaluation framework comparing CDMOs across key criteria:

Score each CDMO objectively against these criteria. This systematic approach reduces bias and facilitates stakeholder alignment on the final selection.

Frequently Asked Questions (FAQ)

What are peptides used for in the pharmaceutical industry?

Peptides serve as therapeutic agents for diverse medical conditions including metabolic disorders (diabetes, obesity), cancer, rare gastrointestinal diseases, cardiovascular conditions, neurological disorders, infectious diseases, and hormone replacement therapy. Their high specificity and ability to target cell receptors with precision make them valuable alternatives to traditional small molecule drugs and biologics.

What is a peptide CDMO?

A peptide CDMO (Contract Development and Manufacturing Organization) is a specialized service provider that partners with pharmaceutical and biotech companies to develop and manufacture peptide-based drug substances and drug products under GMP conditions. Peptide CDMOs combine solid-phase and solution-phase synthesis expertise with downstream purification, analytical characterization, and formulation development capabilities, supporting programs from IND-enabling clinical supply through commercial-scale manufacturing.

What are the four types of peptides?

Peptide therapeutics can be categorized in multiple ways. One classification includes: (1) Native peptides—identical to naturally occurring sequences; (2) Analog peptides—modified versions with amino acid substitutions to improve properties; (3) Heterologous peptides—derived from different species; and (4) Synthetic peptides—designed de novo without natural templates. Another classification distinguishes peptide hormones, antimicrobial peptides, neuropeptides, and signal peptides based on biological function.

How are peptide drugs manufactured?

Peptide drugs are manufactured primarily through solid-phase peptide synthesis (SPPS), where amino acids are sequentially added to a growing peptide chain attached to a solid resin support. Alternative methods include liquid-phase synthesis and recombinant DNA technology using biological expression systems. After synthesis, peptides undergo purification via high-performance liquid chromatography, followed by lyophilization (freeze-drying) and rigorous analytical testing before formulation into drug products.

How are therapeutic peptides manufactured at a CDMO?

Therapeutic peptide manufacturing at a CDMO begins with solid-phase peptide synthesis, in which amino acids are added sequentially to a growing chain anchored on a solid resin support. Following chain assembly, the peptide is cleaved from the resin, deprotected, and subjected to preparative HPLC purification to remove truncated sequences, deletion variants, and process-related impurities. The purified peptide is then characterized by mass spectrometry, amino acid analysis, and purity testing before being formulated into the drug product — typically a lyophilized solid or liquid injectable — and subjected to full GMP release testing before release for clinical or commercial use.

What is the difference between API and peptide?

Active Pharmaceutical Ingredient (API) refers to any biologically active component in a drug formulation responsible for therapeutic effect. A peptide API is a specific type of API consisting of amino acid chains. In other words, “peptide” describes the chemical class (amino acid polymers), while “API” indicates the functional role as the active drug substance. APIs can be small molecules, biologics, or peptides. Peptides represent a distinct category of APIs with unique manufacturing requirements, typically produced through chemical synthesis or biotechnology rather than traditional chemical synthesis used for most small molecule APIs.