Antibody-drug conjugates (ADCs) are precision oncology biologics that link a targeting monoclonal antibody to a potent cytotoxic payload via a chemical linker. Their multi-step, hazardous manufacturing process has made specialist ADC CDMO manufacturing one of the fastest-growing and most technically demanding segments in pharmaceutical outsourcing — and a critical strategic priority for both large pharma and emerging biotech sponsors.

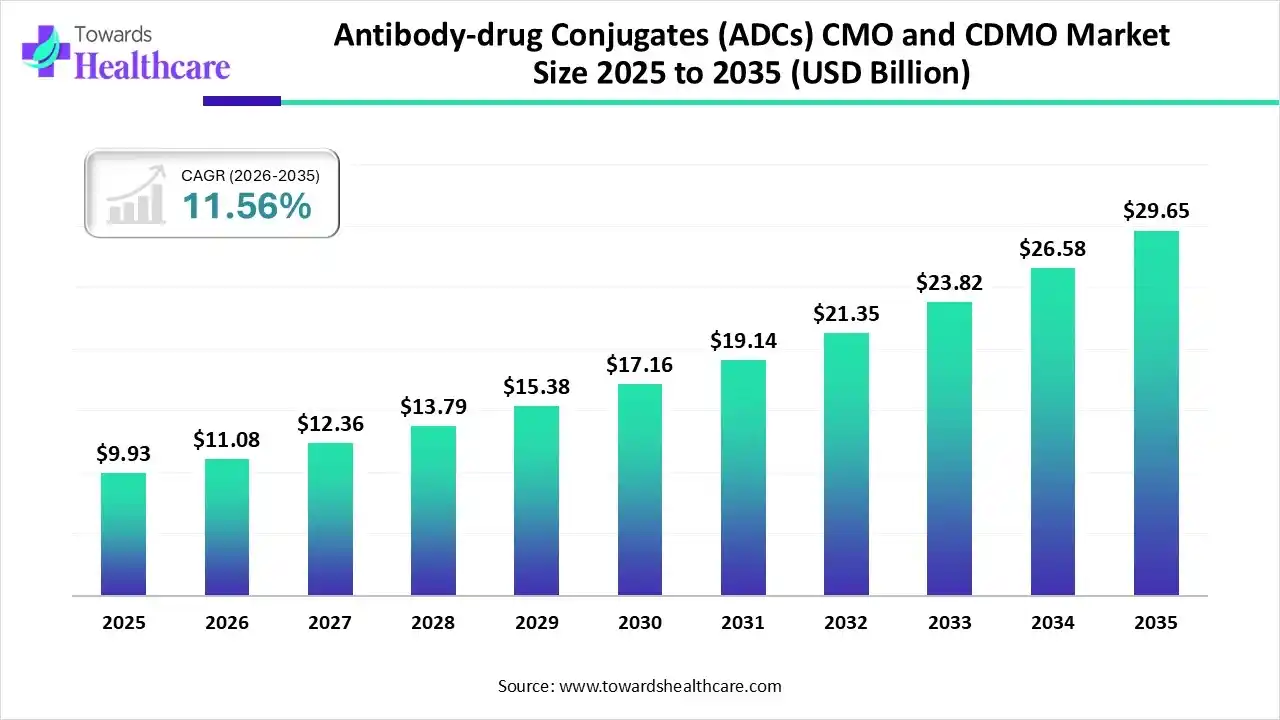

The global ADC contract manufacturing market reached an estimated USD 11.08 billion in 2026 and is projected to expand to approximately USD 29.65 billion by 2035, at a CAGR of 11.56%, according to Towards Healthcare (2026).

The market is expanding steadily, fueled by rising oncology pipelines growing outsourcing of complex biologics, the need for specialized conjugation capabilities, and increasing investments in scalable, compliant manufacturing infrastructure worldwide.

Few vantage points on this market are more instructive than those of senior leaders inside specialist CDMOs. Campbell Bunce, Chief Scientific Officer at Abzena — a CDMO with manufacturing sites in San Diego and Bristol, Pennsylvania — captures the moment well. Speaking on the PharmaSource podcast, he described the trajectory of ADCs and next-generation bioconjugates as one that has fundamentally reshaped the manufacturing landscape.

“Twenty years ago, who knew that ADCs and next-generation bioconjugates were going to be so exciting, so successful?”

— Campbell Bunce, Chief Scientific Officer, Abzena

That success is now placing acute pressure on available manufacturing capacity. Three macro trends are reshaping the ADC CDMO landscape heading into 2026:

- Pipeline maturity and commercial pressure: More than 200 ADC candidates are in active clinical development, targeting over 50 antigens, with 41 assets already in Phase III. This translates directly into sustained pressure on GMP conjugation capacity, driving earlier outsourcing decisions and longer-term capacity reservation agreements.

- Capacity consolidation and integration: Major CDMOs are investing at scale in end-to-end ADC infrastructure — integrating antibody production, linker-payload synthesis, bioconjugation, and aseptic fill-finish under a single quality system — to capture the integrated-partner preference of large pharma sponsors.

- Geographic reshaping and US on-shoring: North America accounted for approximately 42%-45% of the ADC CDMO market in 2025. Geopolitical pressure to on-shore pharmaceutical manufacturing is intensifying domestic demand, particularly for US-based conjugation capacity. As Bunce noted of Abzena’s US positioning: there are not many manufacturers of ADCs in the US, making domestic ADC CDMO capacity a genuinely scarce resource.

What are Antibody-Drug Conjugates?

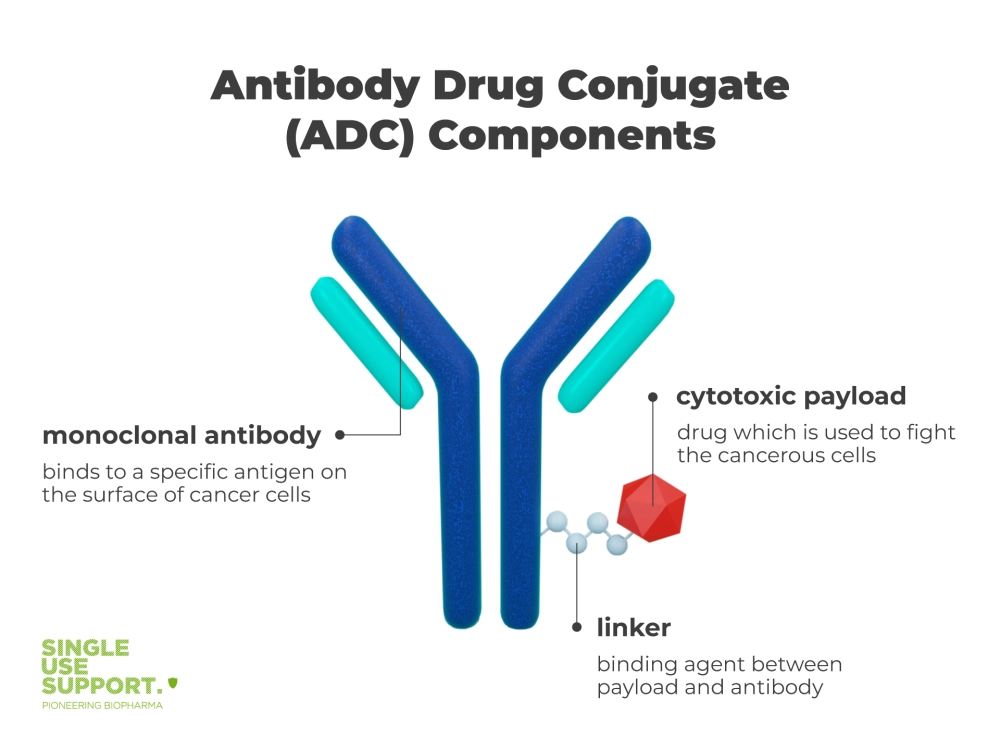

An antibody-drug conjugate is a targeted biopharmaceutical built from three components: a monoclonal antibody that identifies and binds to a tumor-specific antigen, a highly potent cytotoxic payload that kills the target cell, and a chemical linker that controls payload delivery. Manufacturing all three components in a coordinated, GMP-compliant process — while managing the extreme hazard of cytotoxic payloads — is the core challenge that drives outsourcing to specialist CDMOs.

At their core, ADCs consist of three primary components:

1. Monoclonal antibody: This serves as the targeting mechanism, designed to recognise and bind to specific antigens expressed on the surface of cancer cells.

2. Cytotoxic payload: This is a potent small molecule drug, often too toxic for systemic administration on its own, which is responsible for killing the cancer cells once internalised.

3. Linker: This chemical structure connects the antibody to the cytotoxic payload, playing a crucial role in the stability of the ADC in circulation and the controlled release of the payload once inside the target cell.

The seamless integration of these components results in a ‘magic bullet’ approach to cancer treatment, aiming to overcome the limitations of traditional chemotherapy by enhancing efficacy and reducing systemic toxicity.

The antibody component (most commonly IgG1 or IgG4) is produced via mammalian cell culture, then conjugated to the payload through the linker in a tightly controlled chemical step. The drug-to-antibody ratio (DAR) — the average number of payload molecules per antibody — is a critical quality attribute governing both efficacy and toxicity. Achieving a highly stable and uniform DAR is one of the defining technical challenges in ADC manufacturing and a core differentiator for specialist CDMOs.

Bunce describes the DAR stability problem directly in the context of Abzena’s proprietary ThioBridge™ conjugation platform, developed specifically to address one of the sector’s most persistent quality challenges:

“With ADCs, there’s a big issue of stability in vivo and off-target toxicity. Using the expertise within the business, the team looked at how they could overcome that and developed ThioBridge™. We generate a highly stable, highly uniform drug-to-antibody ratio form of the ADC. It’s scalable, and we’ve seen it perform better in vivo.”— Campbell Bunce, CSO, Abzena

Latest ADC News-

ADC payloads are among the most hazardous active pharmaceutical ingredients in pharmaceutical manufacturing, with occupational exposure limits for compounds such as auristatins, maytansinoids, and camptothecin derivatives falling as low as 1 ng/m³. This extreme potency demands purpose-built containment infrastructure — negative-pressure isolators, dedicated hot suites, engineering controls, and continuous environmental monitoring — well beyond standard HPAPI requirements.

ADCs are predominantly developed for oncology. Nineteen products have received regulatory approval globally as of 2026, with approved indications spanning breast cancer, bladder cancer, cervical cancer, acute myeloid leukemia, diffuse large B-cell lymphoma, multiple myeloma, and others. HER2-directed and Trop-2-directed ADCs are the leading target classes by commercial revenue, with Enhertu generating approximately USD 3.75 billion in 2024 revenue according to Roots Analysis (2026).

Bunce points to Novartis’s approximately USD 12 billion acquisition of Avidity Biosciences as further evidence of the sector’s commercial momentum and the strategic value being placed on companies with deep AOC and ADC expertise.

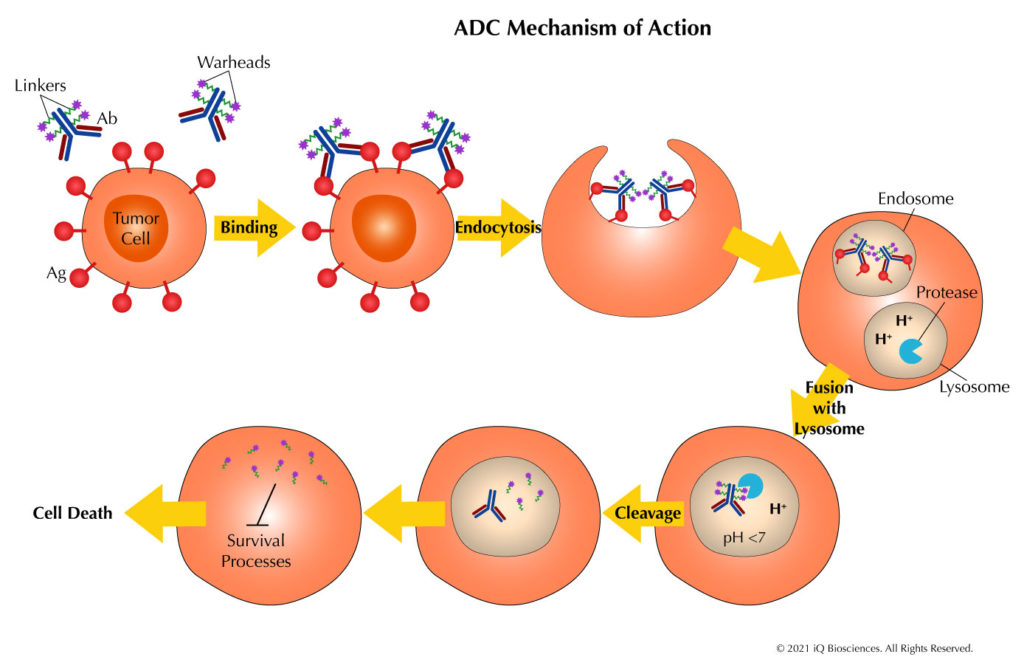

How do ADCs work?

The mechanism of action for ADCs involves several key steps, each critical to their therapeutic efficacy:

1. Targeted Binding: The monoclonal antibody component of the ADC selectively binds to specific antigens overexpressed on the surface of cancer cells. This targeting mechanism is crucial for the precision of ADC therapy.

2. Internalisation: Once bound to the target antigen, the ADC-antigen complex is internalised into the cancer cell through endocytosis. This process effectively delivers the entire ADC inside the cell.

3. Lysosomal Processing: Inside the cell, the ADC-antigen complex is typically trafficked to lysosomes, where the acidic environment and specific enzymes begin to break down the complex.

4. Payload Release: The linker, designed to be stable in circulation but labile under specific intracellular conditions, is cleaved. This releases the cytotoxic payload within the cancer cell.

5. Cell Death: The free cytotoxic drug then exerts its cell-killing effects, typically by disrupting critical cellular processes such as DNA replication or microtubule assembly, leading to apoptosis of the cancer cell.

6. Bystander Effect: In some cases, depending on the nature of the payload and linker, the released cytotoxic drug may also diffuse into neighbouring cells, potentially killing nearby cancer cells that may not express the target antigen.

This multi-step process allows ADCs to deliver potent cytotoxic agents specifically to cancer cells, potentially maximising efficacy whilst minimising systemic toxicity.